By

![]()

![]()

![]()

Life can be hard sometimes, and financial troubles can make it even more difficult. If you are a home owner with financial difficulties, you may find yourself going into foreclosure, being evicted, filing for bankruptcy, or doing a short sale. But what do all of these daunting terms mean? And what are your options? Save yourself some panic and find out below.

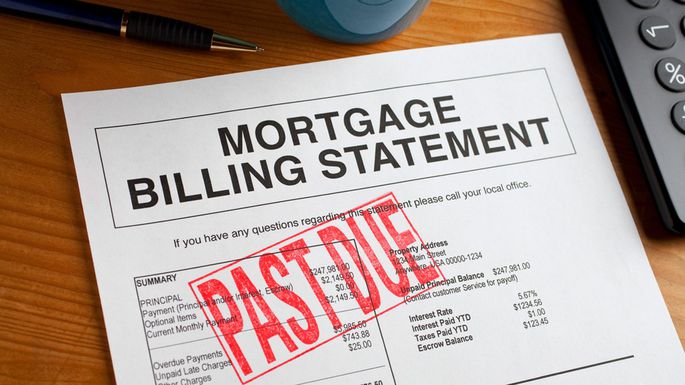

It is not uncommon to struggle with making payments on your mortgage, however, if you fall too far behind, you will face some consequences. When you sign a mortgage you are entering a legally-binding contract with the lender. You have agreed to repay the lender in full according to their terms. If you stop making payments then you are breaching the contract and that is where the trouble starts. After three to six months of missing payments, you will receive either a “notice of default” or a notice of complaint, depending on your state. This notice lets you know that your lender has filed with either the court or the county recorder’s office and that eviction may be on the horizon if the proceedings go through. It also means that you are officially entering into the pre-foreclosure period and it is time to take action.

The pre-foreclosure period can last 30 to 120 days and this time gives you the opportunity to renegotiate with your lender and come up with a solution. The first thing to do during this period is to read everything that you have been sent by your lender. Many lenders will include foreclosure prevention options on their first few late payment notices, some of these may still be an option and it is important to be educated on them before you begin negotiations.

If you live in Connecticut, Delaware, DC, Florida, Hawaii, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, New Jersey, New Mexico, New York, North Dakota, Ohio, Oklahoma, Pennsylvania, South Carolina, Vermont, or Wisconsin, you live in a judicial foreclosure state. This means that your lender has to file a lawsuit against you in court and the process will likely take longer, giving you more time to navigate your options. In non-judicial foreclosure states, filing with the court is not a requirement. Knowing your state’s foreclosure laws will give you the clearest picture of your options.

Once you feel educated on your rights and the local laws, it is time to call your lender. Because home repossession is time-consuming and expensive, most lenders would rather work with you to come up a solution so be open-minded throughout the process. There are several options they may offer you, with refinancing, a repayment plan, forbearance, and loan modification, being some of the most popular.

If you are offered the option of refinancing, the lender will allow you to take out a new loan on your property to cover the missed payments. This new loan will come with new interest rates and terms however will not negatively affect your credit score and can produce more manageable monthly payments.

A repayment plan will allow you to reconfigure, and restart, your monthly payments into a plan that fits your budget. You will however have to make up your missed payments and it will likely take longer to pay off your mortgage. The terms of your mortgage will not change, you will just have a different path to meeting them.

If your lender agrees to suspend your mortgage payments until you are back on your feet, they are agreeing to a forbearance. This temporary suspension aims to give you time to get money together and the missed payments will be moved to the end of your loan.

Much like a repayment plan, a loan modification works to make monthly payments more manageable. Your lender will change the length, interest rate, and amount due on your current loan in order to make up for the missed payments and avoid repossession.

The above options may be confusing and it can be difficult to decipher which is the best step for you and your situation. If you are still struggling with your options, speaking with a HUD-approved counselor may be a helpful tool. There are many free, federally-funded agencies that are here to help in difficult foreclosure situations and their professional advice may put you on the right path.

Some lenders may not offer any of the above options, or you just might not be able to financially handle the terms that they are negotiating. If this is the case, filing for bankruptcy may be your next option. Full disclosure, filing for bankruptcy will heavily impact your credit score which can make purchases further down the line a struggle, but it can also delay foreclosure and reduce your debt. Depending on your current income, you will either file for Chapter Seven bankruptcy or Chapter 13 bankruptcy. If you file for Chapter Seven, all debt will be removed, however a court-appointed trustee will be allowed to sell off any and all of your non-exempt property in order to pay back the creditors. If you file for Chapter 13, you will not lose any of your property, however will have to pay back a portion, maybe even all, of your debt in a repayment plan. Filing for either of these bankruptcies will halt the foreclosure proceedings.

Your final option when falling behind on payments and facing foreclosure is doing a short sale. A short sale is for those who do not feel like they will be able to repay their mortgage, even when using any of the above mentioned options. A short sale process is much like the settlement process on any regular sale. You will find an agent and list your home in the hopes that someone will buy it. Unlike a regular settlement, you are not the person choosing who buys the house, that choice comes down to the lender. In a short sale you are selling the home for less money than you currently owe to the lender, therefore the lender must approve all offers on the home. Receiving lender approval for a short sale can take some time so be prepared to be patient if you feel this is the best option for you.

Find out how Champion Title & Settlements, Inc. can assist you with your foreclosure sales, refinances, and short sales at www.championtitle.com